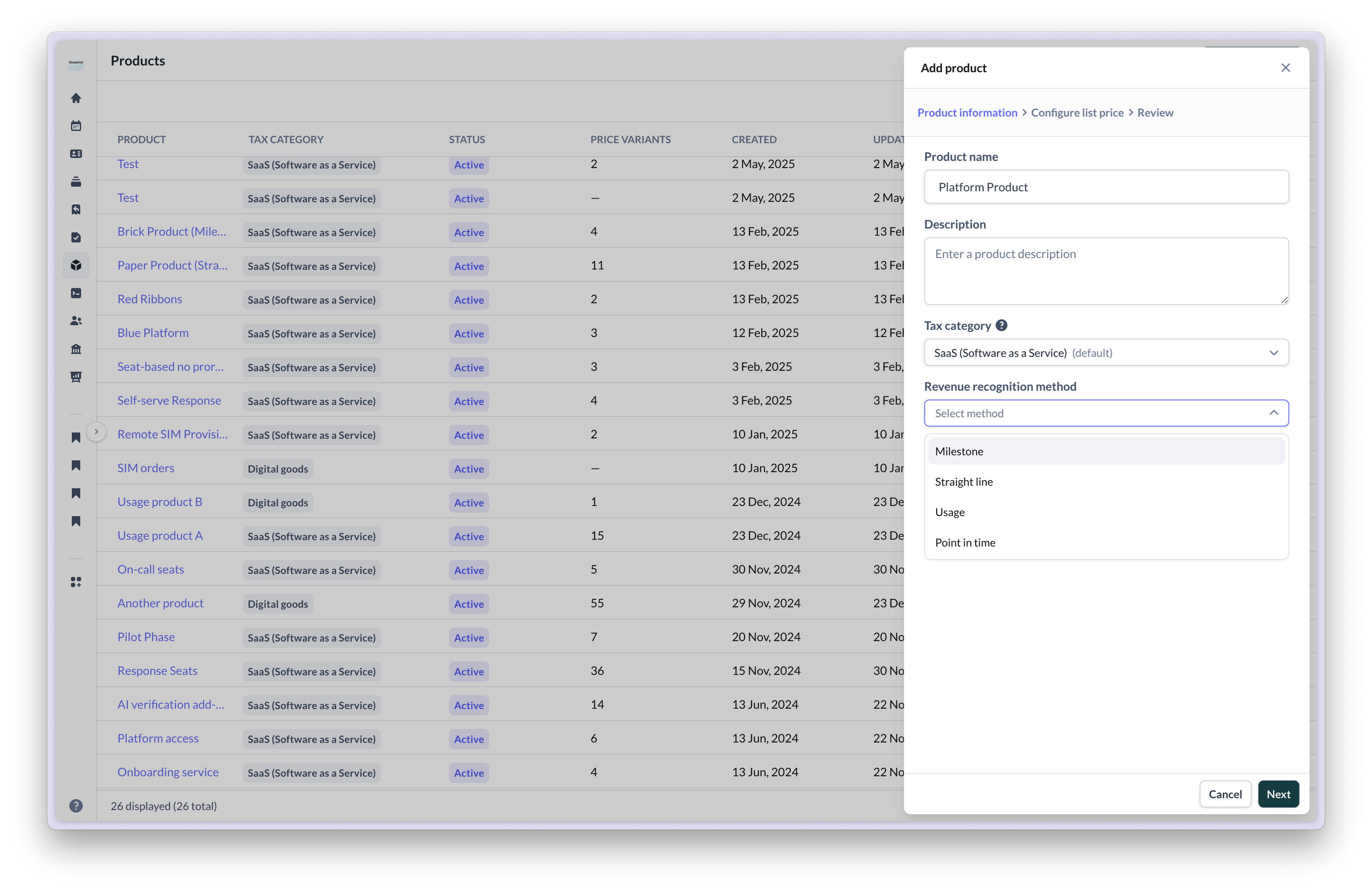

Recognition methods can be set per product in your product catalog and overwritten on individual invoice line items.

Straight-line recognition

Straight-line recognition spreads the contracted amount evenly across the service period. Use it for subscriptions, licenses, and ongoing support. Sequence offers three straight-line allocation methods. They all recognize the same total and give every full month an equal amount — they differ only in how the part-months at the start and end of the service period are prorated. By default, Sequence uses the Prorate first & last with daily rate, even months method; see Allocation methods to compare all three.In-advance billing with straight-line recognition

For subscriptions paid upfront:-

On invoice date: Revenue is deferred

- Debit: Billed Revenue (+$12,000)

- Credit: Deferred Revenue (+$12,000)

-

Daily recognition: Revenue is recognized over time

- Debit: Deferred Revenue (-$33/day)

- Credit: Recognized Revenue (+$33/day)

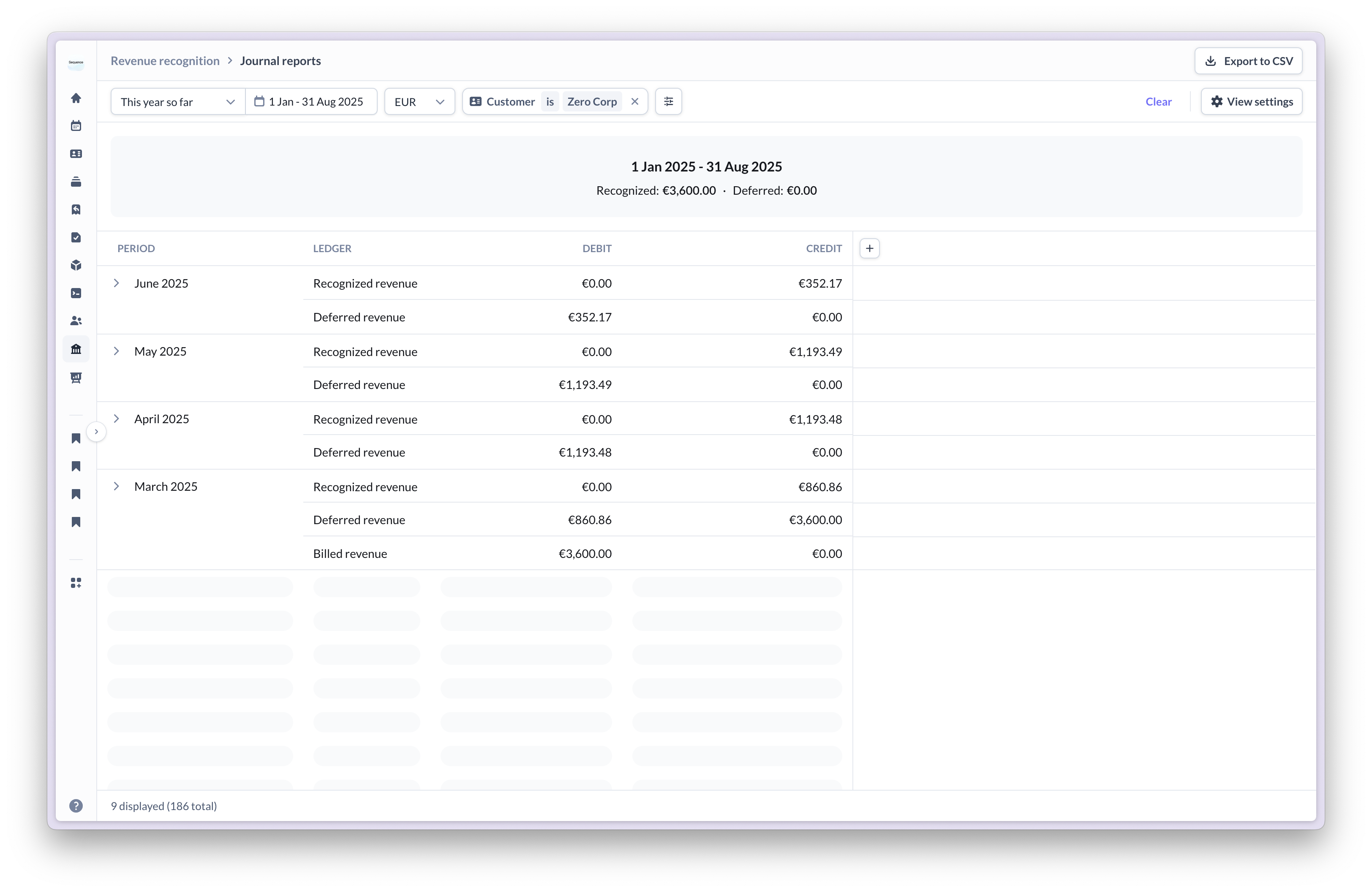

Worked example: Quarterly in-advance billing

Worked example: Quarterly in-advance billing

Scenario

- Amount: €3,600.00 per quarter

- Billing: Quarterly in advance

- Service period: March 10 - June 9, 2025 (92 days total)

-

On invoice date: Full amount deferred

- Debit: Billed Revenue (+€3,600)

- Credit: Deferred Revenue (+€3,600)

-

Monthly recognition totals:

- March (22 days): €860.86 recognized (€3,600 ÷ 92 days * 22 days)

- April (30 days): €1,193.48 recognized (allocated evenly between full months)

- May (31 days): €1,193.49 recognized (allocated evenly between full months, with remainder)

- June (9 days): €352.17 recognized (€3,600 ÷ 92 days * 9 days)

-

Daily recognition granularity: Revenue recognized evenly as services are delivered

- Daily amount: e.g. March €39.13 per day (€860.86 ÷ 22 days)

- Daily journal: Debit Deferred Revenue (-€39.13), Credit Recognized Revenue (+€39.13)

This example uses Sequence’s default Prorate first & last with daily rate, even months allocation method: the part-months (March and June) are paid at the contract’s daily rate, and the full months (April, May) share the rest evenly. See Allocation methods to compare the alternatives.

In-arrears billing with straight-line recognition

For services billed after delivery:-

During service period: Revenue is recognized as unbilled

- Debit: Unbilled Revenue (+monthly amount)

- Credit: Recognized Revenue (+monthly amount)

-

On invoice date: Unbilled revenue becomes billed

- Debit: Billed Revenue (+monthly amount)

- Credit: Unbilled Revenue (-monthly amount)

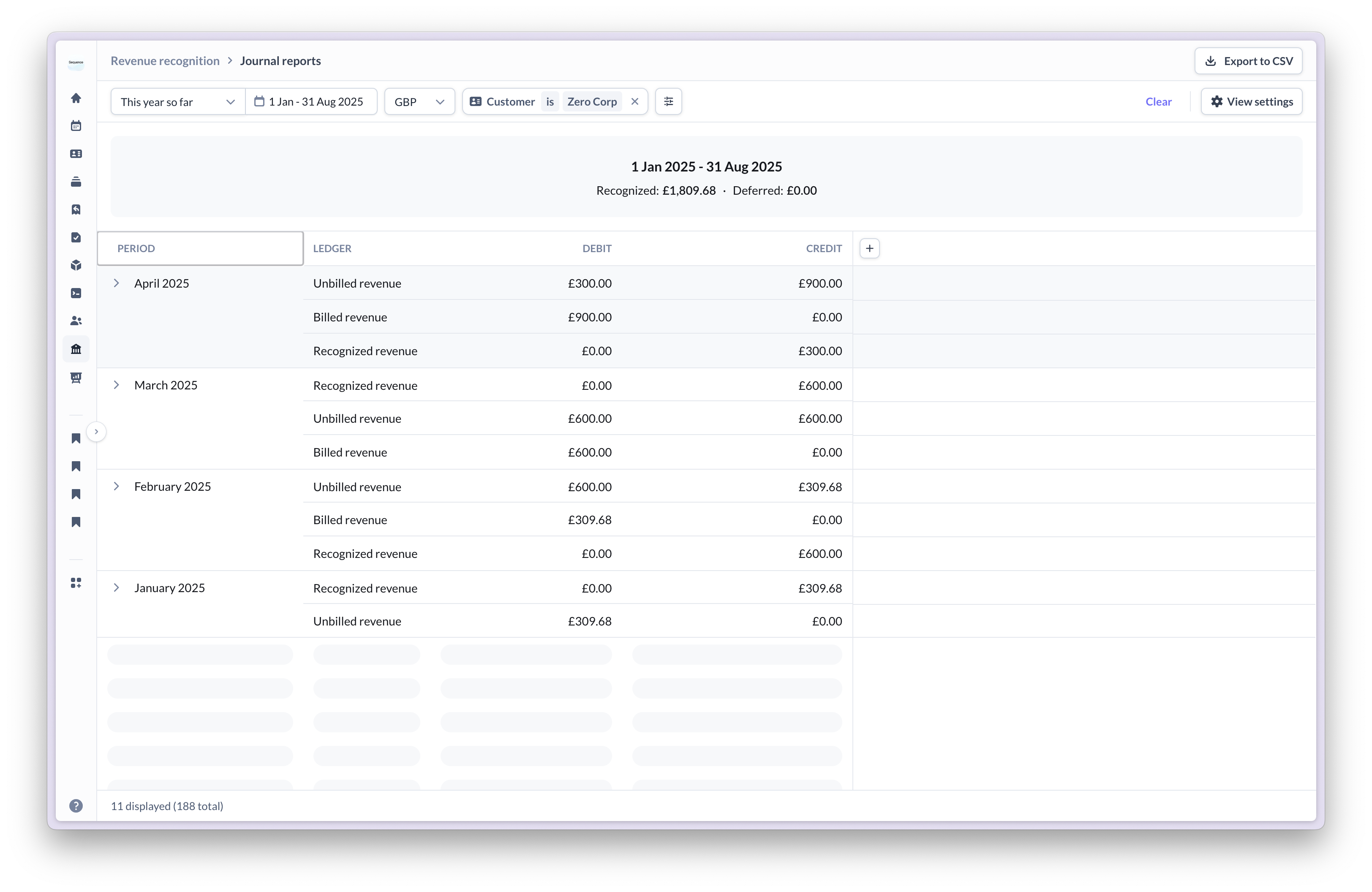

Worked example: Monthly arrears billing with proration

Worked example: Monthly arrears billing with proration

Scenario

- Amount: £600.00 per month

- Billing: Monthly in arrears

- Service period: January 16 - April 15, 2025 (90 days total)

-

Monthly recognition totals:

- January (16 days): £309.68 recognized, invoiced February 1st

- February (28 days): £600.00 recognized, invoiced March 1st

- March (31 days): £600.00 recognized, invoiced April 1st

- April (15 days): £300.00 recognized, invoiced April 16th

-

Daily recognition granularity: Revenue recognized evenly as services are delivered

- Daily amount: £600.00 monthly amount ÷ days in that month

- Daily journal: Debit Unbilled Revenue (+daily amount), Credit Recognized Revenue (+daily amount)

-

On each invoice date: Unbilled revenue becomes billed

- Monthly journal: Debit Billed Revenue (+monthly amount), Credit Unbilled Revenue (-monthly amount)

This example uses Sequence’s default allocation method. First and last months are prorated based on actual days in the service period. See Allocation methods for how the alternatives differ.

Allocation methods

Sequence offers three straight-line allocation methods. All recognize the same total and give every full month an equal amount — they differ only in how the partial months at the start and end of the service period are prorated.- Prorate first & last with daily rate, even months (default)

- Even months, prorate first, balance last

- Even months, prorate first & last

- Method 1

- Method 2

- Method 3

*The last full month absorbs the rounding remainder.How it works: The first and last part-months are paid at the contract’s overall daily rate (total ÷ days); the remaining revenue is split evenly across the full months. The last full month absorbs any rounding remainder.When to use: when you want day-level precision at the start and end of a contract — for example, aligning to a specific go-live date.

Usage-based recognition

Usage-based recognition captures revenue as customers consume. Use it for API calls, data processing, and consumption pricing. Revenue is recognized at the end of the period based on actual usage during that period, regardless of when the invoice is issued.In-arrears usage-based billing

Most usage-based pricing follows this pattern:-

As usage occurs: Revenue is recognized in full at the end of the period

- Debit: Unbilled Revenue (+usage amount)

- Credit: Recognized Revenue (+usage amount)

-

On invoice date: Unbilled revenue becomes billed

- Debit: Billed Revenue (+usage amount)

- Credit: Unbilled Revenue (-usage amount)

Worked example: Monthly usage-based billing in arrears

Worked example: Monthly usage-based billing in arrears

Scenario

- Product: Usage Product at $10.00 per unit

- Billing: Monthly in arrears

- Service period: May 1 - May 31, 2025

- Usage: 4 events during May

-

During service period: Usage events tracked but not yet recognized

- 4 events × $10.00 = $40.00 total usage for May

-

End of service period (May 31st): All usage recognized in single journal

- Journal: Debit Unbilled Revenue (+$40.00), Credit Recognized Revenue (+$40.00)

-

On invoice date (June 1st): Unbilled revenue becomes billed

- Invoice amount: $40.00 for May usage

- Journal: Debit Billed Revenue (+$40.00), Credit Unbilled Revenue (-$40.00)

Usage-based recognition captures revenue as value is delivered through actual consumption, regardless of billing timing.

Point-in-time recognition

Point-in-time recognition captures the full amount on a specific date, typically the service delivery date. Use it for implementation fees, setup charges, and one-time deliverables.Point in time recognition is only available as a recognition method when the service period of the item is a single day.

- Full $5,000 recognized on delivery date

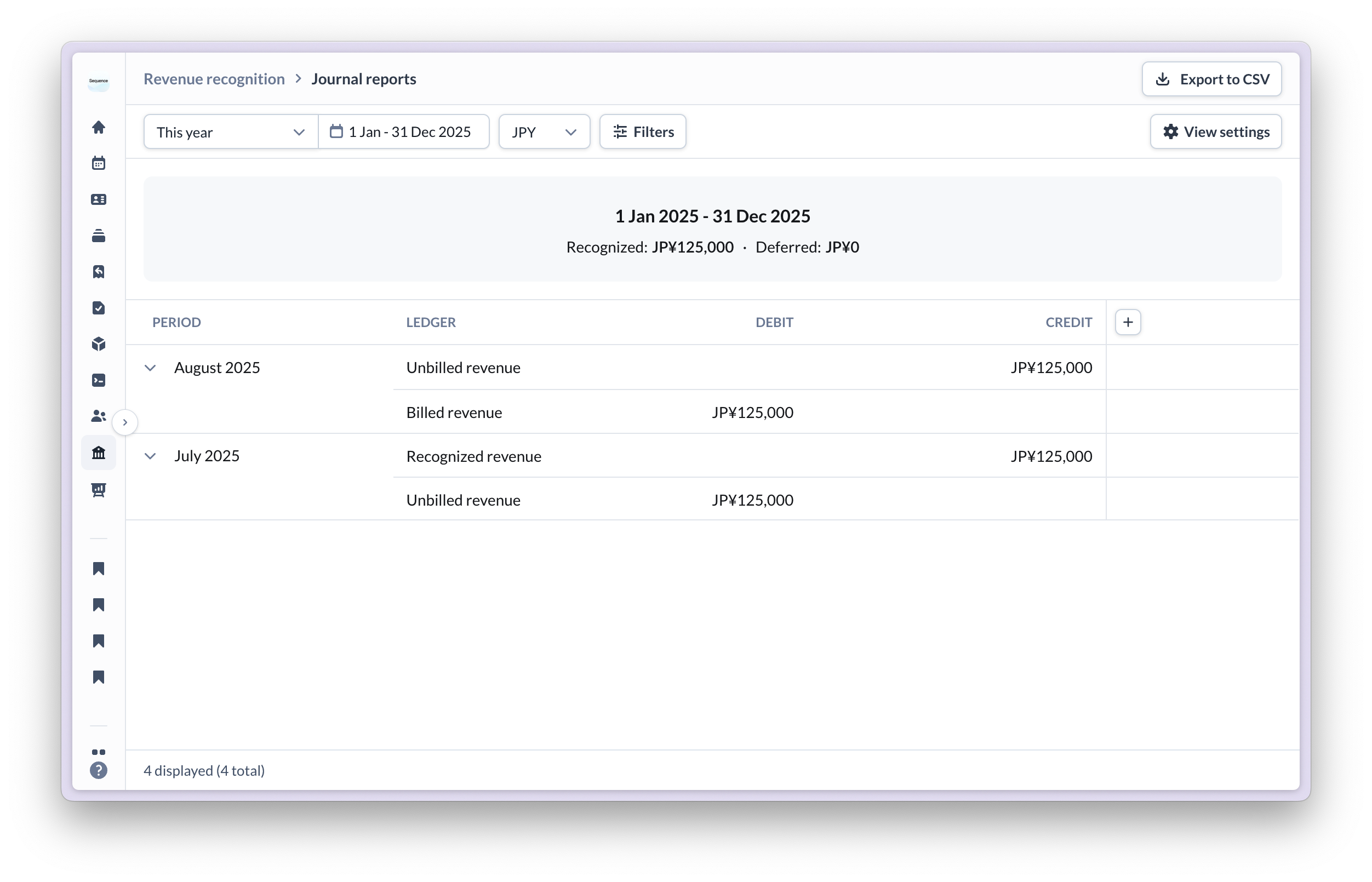

Worked example: In-arrears point-in-time billing

Worked example: In-arrears point-in-time billing

Scenario

- Amount: ¥125,000

- Service period: July 10, 2025 (single day)

- Invoice date: August 7, 2025

- Recognition method: Point-in-time

-

On service delivery date (July 10th): Full amount recognized as unbilled

- Journal: Debit Unbilled Revenue (+¥125,000), Credit Recognized Revenue (+¥125,000)

-

On invoice date (August 7th): Unbilled revenue becomes billed

- Journal: Debit Billed Revenue (+¥125,000), Credit Unbilled Revenue (-¥125,000)

Point-in-time recognition captures the full revenue immediately when the service is delivered, regardless of the date the invoice is issued.

In-advance point-in-time

For fees paid before delivery: On invoice date: Revenue is recognized immediately- Debit: Billed Revenue (+$5,000)

- Credit: Recognized Revenue (+$5,000)

Point-in-time recognition creates a single journal entry on the invoice accounting date, regardless of billing timing. Revenue is recognized immediately rather than deferred.

In-arrears point-in-time

For fees billed after delivery:-

On delivery date: Revenue is recognized as unbilled

- Debit: Unbilled Revenue (+$5,000)

- Credit: Recognized Revenue (+$5,000)

-

On invoice date: Unbilled revenue becomes billed

- Debit: Billed Revenue (+$5,000)

- Credit: Unbilled Revenue (-$5,000)

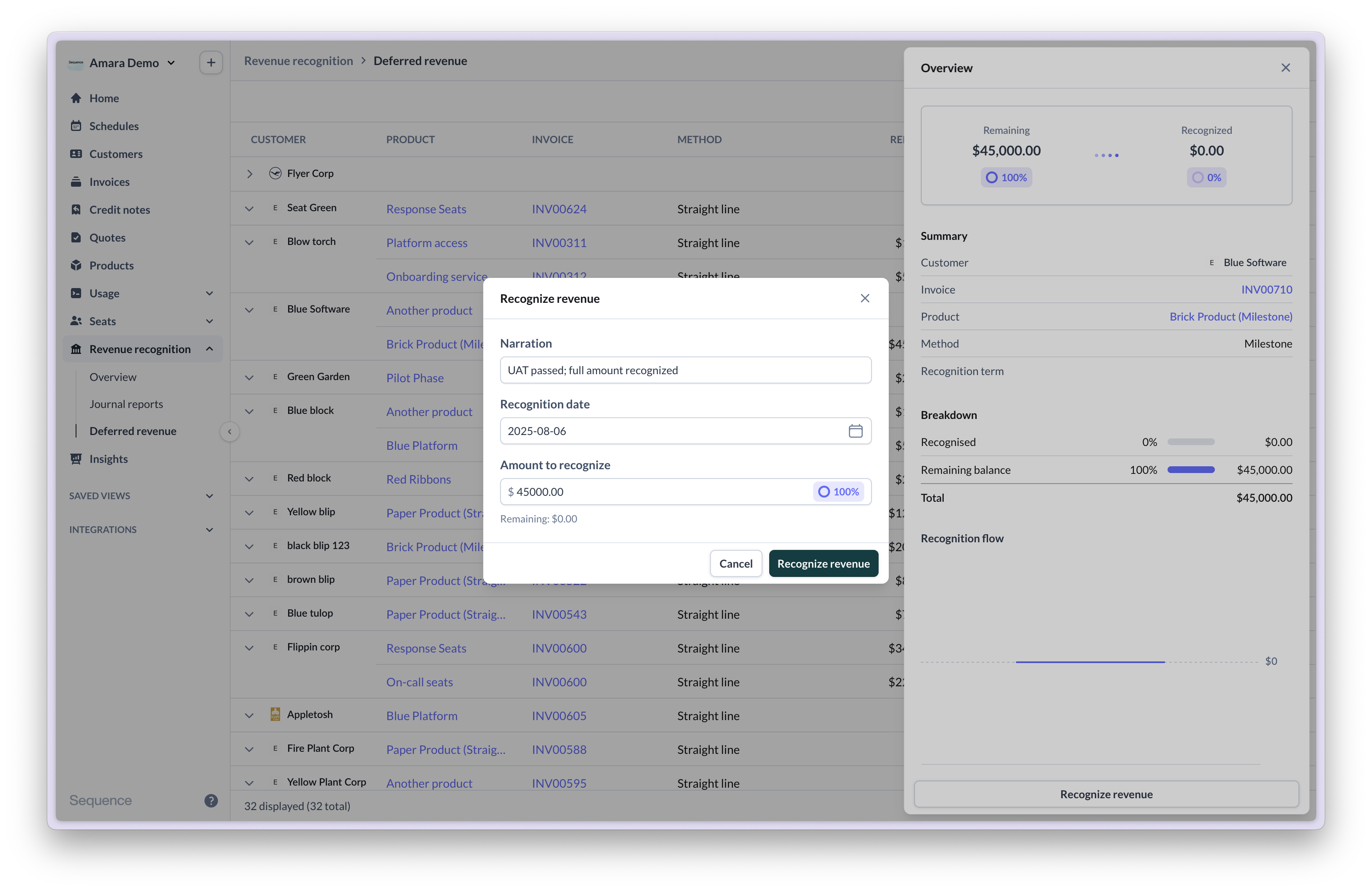

Milestone-based recognition

Milestone recognition releases revenue only when milestones are marked complete. Use it for project work with specific deliverables, such as consulting engagements, custom development, or phased implementations. Recognition timing tracks actual delivery rather than a fixed schedule. Example: $45,000 project with 2 milestones- Milestone 1 completion: $10,000 recognized

- Milestone 2 completion: $35,000 recognized

Worked example: Custom development project with milestones

Worked example: Custom development project with milestones

Scenario

- Product: Custom software development

- Amount: $45,000 total project fee

- Billing: Invoiced upfront on contract signing

- Invoice date: January 15, 2025

- Service period: January 15 - June 15, 2025

- Milestones:

- Milestone 1: Requirements analysis ($10,000)

- Milestone 2: Development and deployment ($35,000)

-

On invoice date (January 15th): Full amount deferred until milestones complete

- Journal: Debit Billed Revenue (+$45,000), Credit Deferred Revenue (+$45,000)

-

Milestone 1 completed (March 1st): First milestone revenue recognized

- Journal: Debit Deferred Revenue (-$10,000), Credit Recognized Revenue (+$10,000)

- Remaining deferred: $35,000

-

Milestone 2 completed (May 15th): Final milestone revenue recognized

- Journal: Debit Deferred Revenue (-$35,000), Credit Recognized Revenue (+$35,000)

- Project complete: $45,000 total recognized

Milestone recognition provides complete control over revenue timing, ensuring recognition only occurs when specific deliverables are actually completed.

Milestone recognition workflow

-

On invoice date: Revenue is deferred (regardless of billing timing)

- Debit: Billed Revenue (+$45,000)

- Credit: Deferred Revenue (+$45,000)

-

When milestone is marked complete: Revenue is recognized

- Milestone 1: Debit Deferred Revenue (-$10,000), Credit Recognized Revenue (+$10,000)

- Milestone 2: Debit Deferred Revenue (-$35,000), Credit Recognized Revenue (+$35,000)