Discounts

Discounts reduce the transaction price according to ASC 606/IFRS 15 guidelines. Sequence supports two types of discounts with different recognition treatments.Product-level discounts

Product-level discounts appear as negative line items within an existing line item group. They’re netted against the product’s price and recognized using the same method and service period. Example: $1,200 annual subscription with 10% discount- Standard price: $1,200

- Discount: -$120 (within same line group)

- Net recognition: $1,080 over 12 months using straight-line method

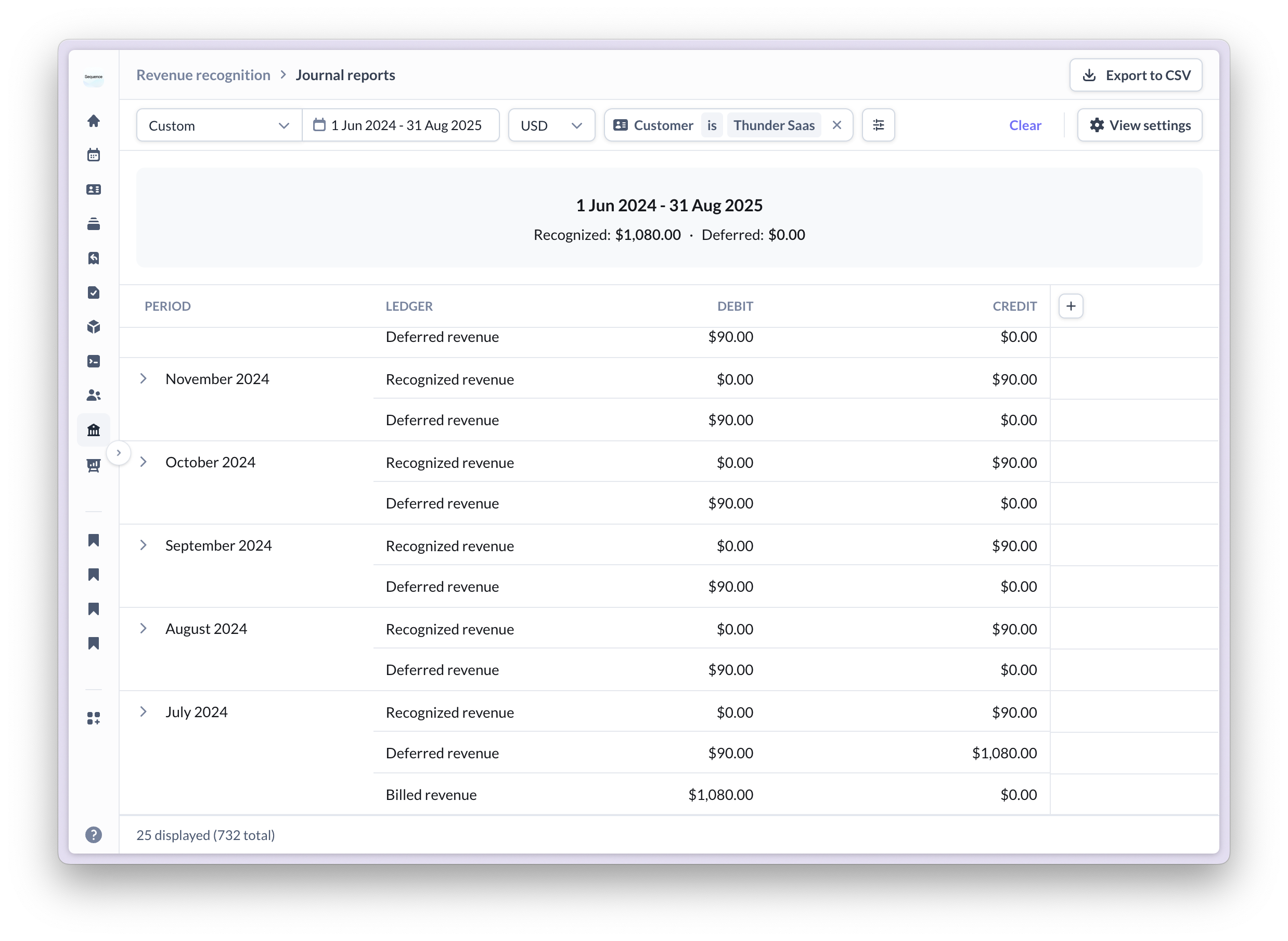

Worked example: Annual subscription with product-level discount

Worked example: Annual subscription with product-level discount

Scenario

- Product: Annual subscription service

- Standard price: $1,200

- Product-level discount: 10% (-$120)

- Net amount: $1,080

- Billing: Annual in advance

- Service period: July 1, 2024 - June 30, 2025 (365 days)

- Recognition method: Straight-line

-

On invoice date (July 1, 2024): Net amount deferred

- Journal: Debit Billed Revenue (+$1,080), Credit Deferred Revenue (+$1,080)

-

Daily recognition: Revenue recognized based on actual days in each month

- Base daily amount: $2.96 per day ($1,080 ÷ 365 days)

- Most days: $2.90 recognized daily

- Month-end adjustments: $3.00 on final day to ensure monthly total of $90

- Example for May 2025: 30 days × $2.90 + 1 day × $3.00 = $90.00

Product-level discounts are netted against the product price and recognized using the same method and timing as the underlying product.

Invoice-level discounts

Invoice-level (global) discounts are separate line item groups with negative amounts. Sequence automatically allocates these discounts pro-rata across all invoice line items based on their standalone selling price. Example: $1,000 total invoice with $100 global discount- Line 1: $800 subscription (gets $80 discount allocation)

- Line 2: $200 setup fee (gets $20 discount allocation)

- Recognition: Each line recognizes its reduced amount using its own recognition method

Allocation is based on standalone selling price (SSP) - the transaction price of each line item - ensuring compliance with ASC 606/IFRS 15 standards.

Credit notes

Credit notes reverse previously recognized revenue. The exact behaviour depends on the credit note variant (invoice-attached, direct, schedule-correction, or standalone) and on the account-level revenue impact mode (cancellation or adjustment). See Credit notes for the full treatment with worked examples. Quick summary:- In cancellation mode (default), the credit note removes future obligations and reverses the deferred balance, before touching recognized revenue if needed.

- In adjustment mode, the original invoice continues recognizing as scheduled, and the credit note posts daily mirror entries that reallocate the reversal across the credit note’s service period.

One-time invoices

One-time invoices recognize revenue based on their service period and selected recognition method, with sensible defaults.Default behaviors

Single-day service period: Point-in-time recognition- Full amount recognized immediately

- Common for ad-hoc charges, refunds, or adjustments

- Revenue spread evenly over the service period

- Partial periods are prorated based on actual days over 365

- Common for project work or time-based services

Customizing invoice line items

You can override any defaults when editing the invoice:- Change recognition method per line item

- Adjust service periods independently

- Select different revenue classifications (arrears/advance)

Minimum fees and true-ups

When usage falls short of committed minimums, Sequence automatically generates true-up line items to ensure the minimum spend is met.True-up creation

When actual usage falls short of the committed minimum, Sequence automatically calculates and adds a true-up line item to meet the shortfall.Worked example: Usage-based billing with minimum fee true-up

Worked example: Usage-based billing with minimum fee true-up

Scenario

- Products: Two usage-based products (A and B)

- Monthly minimum: A$100.00

- Actual usage: A$20.00 (Product A only, Product B had no usage)

- True-up required: A$80.00

- Service period: May 2025

- Billing: Monthly in arrears (June invoice)

-

During May: Usage tracked but not yet recognized

- Product A usage: A$20.00

- Product B usage: A$0.00

-

End of May: Usage and true-up recognized simultaneously

- Usage recognition: Debit Unbilled Revenue (+A$20.00), Credit Recognized Revenue (+A$20.00)

- True-up recognition: Debit Unbilled Revenue (+A$80.00), Credit Recognized Revenue (+A$80.00)

- Total recognized: A$100.00 (meeting minimum requirement)

-

On invoice date (June): All unbilled revenue becomes billed

- Invoice total: A$100.00 (A$20.00 usage + A$80.00 true-up)

- Journal: Debit Billed Revenue (+A$100.00), Credit Unbilled Revenue (-A$100.00)

True-up fees use point-in-time recognition because the service period has already been delivered, ensuring immediate recognition when the shortfall is identified.